When you've been in a car accident, the demand letter you send to the insurance company is your opening salvo. It's the formal document where you lay out your case for compensation—making a clear, fact-based argument about why their insured was at fault, detailing your injuries and financial losses, and stating exactly what you believe is a fair settlement to close the claim.

Why Your Demand Letter Is Your Most Important Tool

Before you start writing, it’s crucial to appreciate the strategic power of this document. A demand letter is so much more than a simple request for money; it's the very foundation of your entire insurance claim. This is your chance to present your side of the story to the insurance adjuster in a structured, professional way, setting the tone for all the negotiations that follow.

A well-crafted letter accomplishes several critical goals at once:

- Establishes Liability: It builds a clear, evidence-based narrative proving their policyholder caused the accident.

- Documents Damages: It meticulously catalogues the full scope of your losses, from hard costs like medical bills to the very real impact of pain and suffering.

- Initiates Negotiation: It signals that you are organized, prepared, and serious about your claim, forcing the adjuster to engage in meaningful settlement talks.

- Prevents Lawsuits: A persuasive letter can often lead to a fair settlement offer, helping you avoid a long, stressful, and expensive court battle.

The Foundation of a Successful Claim

Think of your demand letter as the opening argument in your case. If it's vague, disorganized, or missing evidence, you're giving the adjuster an open invitation to delay, lowball, or flat-out deny your claim. On the other hand, a compelling, well-supported letter commands respect and forces them to take you seriously from day one.

This is more important now than ever, especially as accident-related costs continue to climb. In the United States, bodily injury (BI) claims now make up over 51% of all indemnity payments from insurers. The average cost for a single BI claim has also jumped by 12% to $18,500. As a result, more and more people are turning to structured demand letters to secure fair compensation without needing to file a lawsuit. You can explore these statistics in the full US Auto Insurance Trends Report.

Your goal is not just to ask for money. It's to persuade the adjuster that your demand is reasonable, justified, and backed by undeniable proof. This approach puts you in the driver's seat of the negotiation.

To make a truly persuasive argument, you need to understand the key pieces that make a demand letter work. These components come together to tell a complete and convincing story of the accident and its aftermath.

Key Components of an Effective Demand Letter

To ensure your letter is comprehensive and persuasive, it must include several core elements. Each piece serves a distinct purpose, building on the others to create a powerful, unified argument.

| Component | Purpose | Example Document |

|---|---|---|

| Liability Argument | Clearly establishes who was at fault for the accident. | Police Accident Report |

| Damages Summary | Details all economic and non-economic losses. | Medical Bills, Wage Loss Statement |

| Supporting Evidence | Provides proof for every claim made in the letter. | Photographs, Repair Estimates |

| Settlement Demand | States the specific monetary amount requested. | Final Calculation Summary |

When these components are thoughtfully assembled and backed by solid documentation, your demand letter becomes a tool that can significantly influence the outcome of your claim.

Building an Unshakeable Foundation of Evidence

A demand letter without solid evidence is just an opinion. It’s your story, but it’s not proof. When you back that letter with a robust collection of documents, however, it transforms into an undeniable case that an insurance adjuster simply can't ignore. This is where you shift from just stating your losses to proving them, building a factual foundation that justifies every single dollar you demand.

Your job is to make it as easy as possible for the adjuster to see the facts and validate your claim. Think of yourself as the architect of your case; each piece of evidence is a brick. A well-organized, comprehensive package signals that you're serious and prepared, which almost always paves the way for a smoother negotiation.

The Official Police Report

First things first: get the police report. This document is the cornerstone of your liability argument. It’s an objective, third-party account of what happened, often packed with diagrams, witness statements, and the officer’s initial take on who was at fault. For most adjusters, this is the very first document they'll look at.

You can get a copy from the law enforcement agency that responded to the crash, whether that was the local PD, the sheriff's office, or state patrol. You might have to pay a small administrative fee, but it’s worth every penny. It establishes the core facts right from the get-go.

Documenting Your Medical Journey

Your medical records and bills are the heart of your injury claim. They draw a straight, documented line from the accident to the physical harm you’ve suffered. Simply saying "I was injured" won't cut it. You need to provide the complete, organized file.

Make sure your file includes every relevant document:

- Initial Emergency Room Records: This establishes the immediate impact of the crash.

- Physician’s Notes: These track your diagnosis, treatment plan, and recovery over time.

- Itemized Billing Statements: Don't just send the summary page. Provide detailed lists of every single service from hospitals, clinics, and specialists.

- Prescription Receipts: Proof of the medications required to manage your injuries.

- Physical Therapy Logs: These records document the necessity and duration of your rehab.

An adjuster's primary job is to validate losses. By providing a complete and chronological medical file, you remove any doubt about the extent of your treatment and the associated costs.

Keeping this mountain of paperwork straight can be a real headache. For some practical tips on creating a clear, logical system, you can learn more about how to organize medical records. A professional presentation ensures nothing gets overlooked. https://areslegal.ai/blog/how-to-organize-medical-records

Proving Your Financial Losses

Beyond the medical bills, you have to prove every other financial hit you took. These are the tangible, out-of-pocket expenses that came directly from the accident, and your evidence needs to be crystal clear.

Lost Wage Verification

If you missed time from work, you'll need a letter from your employer on official company letterhead. This should state your job title, your pay rate, and the exact dates you were out because of your injuries. Tucking in some pay stubs from before and after the accident will make this part of your claim even stronger.

Vehicle Damage and Repair Estimates

For your property damage, documentation is just as critical. A good starting point is to collect at least two to three repair estimates from reputable body shops. This shows the adjuster you’ve done your homework. For a truly solid demand letter to insurance company for auto accident, you might also get a professional car appraisal after an accident to properly document the damage and any loss in your vehicle's value.

The Power of Visual Evidence

Finally, never underestimate what a picture is worth. Photos and videos can tell a story in a way documents never will.

Your visual evidence portfolio should be thorough. Include clear images of:

- The accident scene from several different angles.

- The damage to all vehicles involved.

- Your visible injuries (bruises, cuts, casts) as they healed over time.

- Any important details like road signs, traffic lights, or even weather conditions.

These visuals help the adjuster see what happened, adding a powerful human element to the paperwork and making your suffering much more tangible. When you combine this with official reports and financial records, you create a complete and compelling picture that's hard to argue with.

How to Structure Your Letter for Maximum Impact

The way you structure your demand letter is everything. This isn't just about organizing your thoughts; it's about building a fortress of logic—an argument so clear and well-supported that an insurance adjuster has no choice but to take you seriously.

Think of it as telling a story that leads to one inescapable conclusion: your settlement demand is fair. A rambling, emotional letter is easy to ignore. A professional, methodical one gets put right on top of the stack because it shows you mean business. Each section should flow logically into the next, making the adjuster's job easy by giving them everything they need, exactly when they need it.

The Professional Opening

Your letter needs to get straight to the point right from the beginning. A clean, professional opening sets the tone and immediately gives the adjuster the context they need.

Make sure these key details are right at the top:

- Your Contact Information: Full name, address, and phone number.

- Date: The date you send the letter.

- Adjuster's Information: Their full name, title, and the insurance company’s address.

- Claim Details: The claim number, the date of the accident (loss), and the name of their insured.

A simple, direct subject line like, "RE: Demand for Settlement; Claim # [Your Claim Number]" works perfectly. The first sentence should clearly state that this letter is a formal demand for settlement related to the accident caused by their insured.

Constructing the Liability Argument

Once the basics are out of the way, your job is to prove fault. This section should be a concise, fact-based narrative explaining how the accident occurred and why their insured is 100% liable. Leave emotion at the door and stick to the objective facts.

For example, instead of saying, "Your client was driving like a maniac and smashed into me," state the facts: "Your insured, Mr. John Smith, ran the red light at the intersection of Main Street and Oak Avenue, striking my vehicle. This is confirmed by the official police report (No. 12345), which is attached as Exhibit A."

Reference your evidence directly every time. Mention the police report by number, cite witness statements, and even point to the specific traffic laws their driver broke. When you build a case on cold, hard facts, there’s no room for the adjuster to argue about who was at fault.

Your liability argument should be a straightforward account of the facts. The goal is to make it clear that any attempt to assign partial fault to you is baseless and not supported by the evidence.

This structured approach is becoming a global standard. As insurers face rising claims costs, the use of formal demand letters has increased. For example, in the UK, over 70% of auto accident claims now involve a demand letter, with average settlements climbing to £12,000 due to factors like complex vehicle repairs.

Detailing Your Injuries and Medical Treatment

Now that you've established liability, you need to connect the crash directly to your physical injuries. This section is where you walk the adjuster through your medical journey, from the initial impact to your current state of recovery.

Create a chronological summary of every medical interaction. Detail the first trip to the emergency room, all follow-up appointments with specialists, every physical therapy session, and any surgeries or major procedures you underwent. Using specific medical terms like "cervical strain" or "herniated disc" adds a layer of authority. This narrative isn't just a list; it paints a picture of your pain, suffering, and the extensive care you required. If you want a deeper dive into this document's strategic role, check out our guide on https://areslegal.ai/blog/what-is-a-demand-letter.

Itemizing Your Financial Losses

This is where you lay out the cold, hard numbers. You need to provide a clear, itemized list of your economic losses, often called "special damages." Don't just throw a total at the adjuster—break it down line by line so they can see precisely how you calculated your figure.

Your itemized list needs to include:

- Medical Expenses: List each provider (hospital, clinic, pharmacy) with the total amount they billed.

- Lost Wages: Show the math—your hourly rate multiplied by the number of hours you missed. Back this up with a letter from your employer.

- Property Damage: Include the final bill for your car repairs or the assessed value if it was totaled.

- Out-of-Pocket Costs: Don't forget smaller expenses like prescription co-pays or transportation to your appointments.

Putting these figures into a simple table or a neat bulleted list makes them easy for the adjuster to cross-reference with the documents you’ve attached. To help create a top-notch demand letter to insurance company for auto accident, many professionals now use legal document generation software to ensure nothing gets missed. This methodical breakdown of your damages is the foundation of your final demand, making it logical and tough to refute.

Calculating Your Settlement Demand: Finding the Right Number

Figuring out the final number for your demand letter is more art than science. It's a delicate balance. Aim too low, and you're leaving money on the table. Shoot for the moon with an outrageous figure, and the insurance adjuster might just toss your letter in the "unreasonable" pile, shutting down any chance of a good-faith negotiation before it even starts.

The process is a mix of hard math and subjective, but reasoned, judgment. You’ll start with the easy part—tallying up your provable financial losses—and then move into the more nuanced area of valuing your pain and suffering. Let's walk through how to build a final demand amount that is both fair and solid enough to withstand scrutiny.

Start with the Concrete: Your Special Damages

The most straightforward part of your calculation is adding up what lawyers call special damages (or economic damages). These are the tangible, out-of-pocket costs you’ve incurred because of the accident, and they should all have a paper trail. Precision is your friend here.

Your list of special damages needs to be itemized and directly supported by the documents you’ve gathered. Make sure you include:

- Total Medical Bills: This isn't just the big hospital bill. It's the sum of every invoice from every provider—the ambulance, the emergency room, surgeons, your family doctor, physical therapists, and even chiropractors. Don't forget to add in costs for prescriptions and any medical equipment you needed.

- Lost Income: Calculate every dollar of wages you lost because you couldn't work. If you had to burn through sick days or vacation time, include the value of that time, too. You were forced to use a benefit you had earned, and it has a real monetary value.

- Future Lost Earning Capacity: This is a big one. If your injuries are serious enough to prevent you from returning to your old job or working at the same level, this loss can be substantial. You’ll likely need a vocational expert or economist to project this loss over your working life.

- Property Damage: This is the repair or replacement cost for your vehicle and anything else of value inside it that was damaged or destroyed.

Once you add all these up, you have your baseline number. For instance, if you had $15,000 in medical expenses, $4,000 in lost wages, and another $500 in miscellaneous costs, your total special damages come to $19,500.

The Human Cost: Valuing Your General Damages

Now comes the harder part: calculating your general damages. This is the compensation for the non-financial toll the accident took on you—the physical pain, the emotional distress, the sleepless nights, and the overall disruption to your life. Just because these things don't come with a neat price tag doesn't mean they aren't valuable. They are a very real and legitimate part of your claim.

To put a number on this, insurance adjusters often rely on a simple formula as a starting point. The most common one you'll encounter is the multiplier method.

The multiplier method works by taking your total special damages and multiplying that figure by a number, typically between 1.5 and 5. A straightforward injury with a quick recovery might get a 1.5x multiplier, while a catastrophic, life-altering injury could justify a multiplier of 5 or even higher.

The trick isn't just picking a number out of thin air; it's about building a compelling case for the multiplier you choose.

Justifying Your Multiplier

The strength of your argument for a higher multiplier in your demand letter to insurance company for auto accident comes down to how well you can paint a picture of your suffering. You need to connect the dots for the adjuster.

Here are the factors that push a multiplier higher:

- Severity of Injuries: "Hard" injuries like broken bones, herniated discs, or any kind of head trauma will always command a higher multiplier than "soft tissue" injuries like sprains and strains.

- Length of Recovery: A healing process that drags on for a year, requires multiple surgeries, or involves months of grueling physical therapy warrants a much higher number.

- Permanent Impairment: Did the accident leave you with a permanent scar, a limp, chronic pain, or a lasting disability? These long-term consequences are a powerful justification for being on the higher end of the multiplier scale.

- Psychological Trauma: Don't overlook the mental and emotional fallout. If you have documented anxiety, depression, or PTSD from the crash, that significantly increases the value of your general damages.

Let’s go back to our example. The person with $19,500 in special damages had a broken leg that needed surgery and six months of physical therapy. During that time, they were in constant pain, missed their daughter's graduation, and had to give up their weekend hiking passion. Given the surgery, the long recovery, and the impact on their quality of life, a multiplier of 3 is a very reasonable starting point.

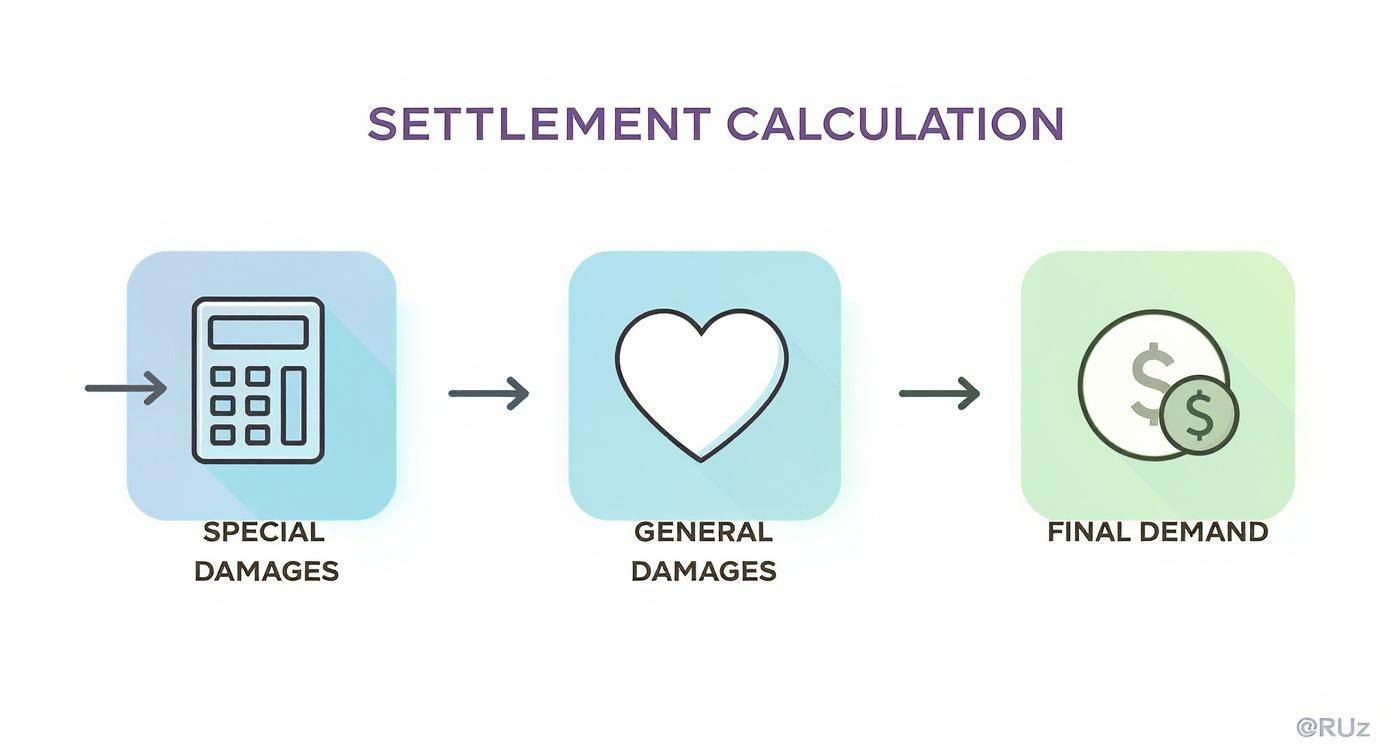

Bringing It All Together for the Final Demand

Once you've landed on a multiplier you can defend, the final math is simple. You just add your special damages and your newly calculated general damages together.

This table shows how the numbers come together using our example.

Sample Settlement Calculation (Multiplier Method)

| Damage Type | Calculation/Example | Amount |

|---|---|---|

| Special Damages | Medical Bills + Lost Wages + Other Costs | $19,500 |

| General Damages | Special Damages ($19,500) x Multiplier (3) | $58,500 |

| Total Demand | Special Damages + General Damages | $78,000 |

The final figure of $78,000 becomes your initial settlement demand. It’s crucial to frame this as your opening position, not your final number, because it builds in room to negotiate. The adjuster will almost certainly counter with a lower offer, and the back-and-forth will begin. By clearly showing your math and justifying every part of your calculation, you’re sending a strong signal that you’ve built a serious, well-supported claim.

Putting It All Together: Assembling and Sending Your Demand Package

You’ve done the hard work of drafting the letter and calculating your demand. Now it's time to assemble a professional package that an insurance adjuster will take seriously. This isn't just about stapling papers together; how you present your claim speaks volumes about your organization and resolve.

The goal here is simple: make the adjuster's job easy. When they can logically connect every statement in your letter to a corresponding piece of evidence, you remove friction and encourage good-faith negotiation. A clean, well-organized package instantly builds your credibility.

Turning Your Evidence Into Exhibits

The most effective way to manage your documentation is to treat it like a formal case file. Think of your demand letter as the story and your evidence as the exhibits that prove it's true. This simple step transforms a messy stack of papers into a professional submission.

I recommend numbering or lettering each piece of evidence so it directly corresponds to where you mention it in the letter. A typical exhibit list might look like this:

- Exhibit A: The official police report.

- Exhibit B: Chronologically ordered medical records.

- Exhibit C: All itemized medical bills.

- Exhibit D: Lost wage verification letter from your employer, plus recent pay stubs.

- Exhibit E: Photos of the vehicle damage and repair estimates.

- Exhibit F: Photos showing your injuries and the recovery process.

Organizing your documents this way makes it incredibly easy for the adjuster to follow along and prevents crucial evidence from being overlooked. A well-structured demand letter to insurance company for auto accident is simply more persuasive.

Pro Tip: Never, ever send your original documents. Always send high-quality copies and keep the originals safely filed away. Originals can get lost in a corporate shuffle, and you must maintain control over your own evidence.

This infographic breaks down how all the pieces of your claim—from medical bills to pain and suffering—come together to form your final demand.

As you can see, the foundation is your provable economic damages, which then helps justify the amount you're seeking for your non-economic damages, like pain and suffering.

The Right Way to Send Your Package

How you deliver the package is just as critical as what’s inside. You absolutely need proof that the insurance company received your demand on a specific date. This creates a legal paper trail and officially starts the clock on their response time.

For this reason, always use a trackable shipping method. The gold standard remains USPS Certified Mail with a return receipt requested. It gives you a tracking number and, more importantly, a physical postcard that is mailed back to you once someone signs for the package—irrefutable proof of delivery.

Steer clear of these common mistakes:

- Standard Mail: A complete no-go. It offers zero proof of delivery.

- Initial Email Submission: Risky. Large attachments get flagged by spam filters, and you lack the formal proof of receipt that certified mail provides.

- Generic Address: Don't send it to a general corporate PO Box. Address it directly to the assigned claims adjuster by name to ensure it lands on the right desk without delay.

By assembling a professional package and sending it with verifiable delivery, you make a powerful final statement. You've presented a thorough, evidence-based claim and are now waiting for their serious consideration. If your case involves a long and complicated medical history, a concise summary can make a huge difference; check out our guide on creating an effective medical record summary to learn more.

Answering Your Top Questions About Auto Accident Demand Letters

Once you've poured all that effort into drafting a solid demand letter, it's natural to have a few lingering questions. Let's tackle some of the most common ones that come up right before you send it off or while you're anxiously waiting for a response.

Getting these answers straight now will help you feel more in control and ready for the negotiation ahead.

When Is the Right Time to Send a Demand Letter?

This is a critical question, and the answer is all about timing. Move too fast, and you could leave a lot of money on the table. Wait too long, and you could lose your right to recover anything at all.

The sweet spot is right after you’ve either finished all your medical treatment or reached what doctors call Maximum Medical Improvement (MMI). This is the point where your condition is stable, and everyone has a clear picture of your long-term prognosis and any future medical needs you might have. If you send the demand before hitting MMI, you simply won't know the full extent—and therefore the full value—of your damages.

But don't forget the clock is ticking. Every state has a statute of limitations for personal injury claims, which is often just two or three years from the accident date. You absolutely must send your letter and either settle or file a lawsuit before that deadline expires.

What if the Insurance Company Gives a Lowball Offer?

First off, don't panic. A low initial offer is completely normal. In fact, you should expect it. The adjuster’s job isn't to be fair; it's to save their company money. Think of it as their opening bid in a negotiation, not a final verdict on your claim.

Your move is to counter their offer calmly and professionally. This isn't the time for emotion; it's a time for facts.

- Start by formally rejecting their offer in writing.

- Briefly restate the most compelling points from your demand.

- Draw a direct line between the evidence you provided and the settlement amount you requested.

- Present a counter-offer that's a bit lower than your initial demand, showing you're ready to negotiate in good faith.

If their offers stay ridiculously low or they just won't budge, that's a strong signal that it might be time to bring in a lawyer.

A lowball offer is an invitation to negotiate, not an insult. Your fact-based, organized response shows you are prepared to stand your ground and signals that they need to come back with a more serious number.

Can I Write a Demand Letter Without a Lawyer?

Yes, you absolutely can, and for many people, it's the right choice. If your accident was straightforward—clear fault, minor injuries, and damages that are easy to add up—you can often handle the process yourself and save on legal fees. This guide is designed to give you the confidence to do just that.

However, some situations are just too complex to go it alone. You should seriously consider hiring a personal injury attorney if your case involves any of the following:

- Serious or permanent injuries that will impact you for years to come.

- A dispute over who was at fault for the accident.

- Massive medical bills or complicated calculations for lost income.

- An insurance company that's dragging its feet, denying your claim outright, or using bad-faith tactics.

A good attorney can often negotiate a much higher settlement, one that more than covers their fee, because insurers take them far more seriously.

Should I Threaten to Sue in My Letter?

You need to show you mean business, but there’s a subtle art to it. Coming out with aggressive, overt threats will likely backfire, causing the adjuster to dig in their heels. The goal is to be firm and assertive, not hostile.

A simple, professional statement at the end of your letter is the most powerful approach. Try something like this:

"If we are unable to reach a fair settlement by the deadline, I will have no choice but to pursue all available legal remedies to protect my interests."

This gets the point across perfectly. It says you're serious and ready to file a lawsuit if needed, but it keeps the tone professional and leaves the door open for a reasonable negotiation. It's the right way to show your resolve.

Drafting a powerful demand letter requires meticulous organization and a deep understanding of your case facts. Ares provides an AI-powered platform built for personal injury firms to automate medical records review and demand letter drafting, turning complex case files into clear, settlement-ready documents in minutes. Eliminate hours of manual work and build stronger cases by visiting the Ares Legal AI website.