You've probably heard the term maximum medical improvement payout, but it's a bit of a misnomer. It’s not some special type of benefit. Instead, it’s the settlement or award you calculate after a doctor declares that your client's medical condition has finally stabilized.

This is the moment of truth in a personal injury case. It signals that no further significant recovery is expected, which is the green light for an attorney to nail down the full, final value of the claim. This includes everything from future medical bills to permanent impairments. MMI is the point where the case pivots from active treatment to final valuation.

Understanding Maximum Medical Improvement

Think of Maximum Medical Improvement (MMI) less as the end of your client's recovery journey and more as the starting line for a proper settlement valuation. It's that critical point when a doctor confirms the client's condition has plateaued, and significant improvement from here on out is unlikely.

Trying to value a claim before MMI is like trying to price a house while the blueprints are still being drawn. You're just guessing.

Once MMI is declared, you finally have the complete picture. It's important to remember that reaching MMI doesn't mean your client is "all better." Far from it. Often, it means they're now living with permanent limitations or will need ongoing care for the rest of their life.

MMI is simply the point where an injured person's medical condition is as good as it's going to get. This allows for a clear and final assessment of permanent disability, which is the foundation for determining the total value of a workers' comp or personal injury claim.

Grasping this concept is the first step in moving from just managing a case to strategically building its value for settlement. The MMI declaration triggers all the crucial valuation work.

Why MMI Is the Cornerstone of Your Valuation

Once a doctor establishes MMI, you can finally calculate the full scope of your client's damages with confidence and accuracy. The stabilization of their condition unlocks your ability to project their long-term needs and losses with a degree of certainty that was impossible before.

Key valuation components you can now lock down include:

- Future Medical Costs: You can now make a solid projection for the cost of ongoing physical therapy, prescription drugs, medical devices, or even potential future surgeries.

- Permanent Impairment Ratings: A physician will assign a rating that quantifies the degree of permanent loss of function, which is a number that directly impacts the settlement value.

- Lost Earning Capacity: With a clear understanding of your client's permanent physical limitations, you can calculate how the injury will impact their ability to earn a living over their entire working life.

- Non-Economic Damages: Arguments for pain and suffering, loss of enjoyment of life, and emotional distress become much stronger once you have medical proof that the injuries are permanent.

This clarity is everything when building a compelling demand package. To do it right, you have to organize and interpret the mountain of medical records leading up to the MMI finding. For a deeper dive into that process, you can learn more about creating an effective medical record chronology in our detailed guide.

Without a firm MMI date from a doctor, any settlement demand you make is built on quicksand. It's pure speculation, and you can bet the defense will exploit that weakness with a lowball offer.

Figuring out when a client has reached Maximum Medical Improvement isn't a simple handshake agreement. It's almost always a battle of competing medical opinions, pitting your client's long-term treating doctor against a physician hand-picked by the insurance company. To protect your client's settlement, you need to understand exactly what drives each side.

Your client's doctor has one priority: getting them as healthy as possible. They’ll declare MMI only when they see the clinical evidence—symptoms have plateaued, pain is manageable and consistent, and more treatment isn't going to move the needle on recovery. Their entire focus is on the patient's well-being.

Insurers, on the other hand, are focused on closing the claim and minimizing their financial exposure. This brings us to the controversial role of the Independent Medical Examiner.

The Independent Medical Examiner vs. The Treating Physician

An Independent Medical Examiner (IME) is a doctor hired by the defense to evaluate your client. Let's be clear: despite the "independent" title, their job is to provide a medical opinion that helps the insurance company's case. Very often, that means arguing for an MMI date that is as early as possible.

The conflict is baked into their motivations:

- The Treating Physician works to get the patient back to their best. They declare MMI only when the healing process has genuinely run its course, an opinion they form after months or even years of direct, hands-on care.

- The Independent Medical Examiner typically conducts a single, brief examination. Their objective is to find anything that can diminish the claim's value, whether that's downplaying the severity of the injuries or declaring MMI has been reached prematurely.

Pushing for an early MMI date is a classic defense tactic. It's designed to cut off temporary disability benefits and pressure your client into a lowball settlement before the true, long-term impact of their injuries is fully understood.

Think of the IME report as a strategic play by the defense, not an objective medical document. Your job is to pick it apart—look for downplayed symptoms, inconsistencies, and any conclusions that clash with the detailed, long-term records of the treating physician.

Your strategy is to elevate the treating doctor's opinion, grounded in a real history of care, while exposing the IME's report for what it usually is: a biased, one-off assessment.

Deconstructing the MMI Report and Impairment Rating

Once MMI is declared, the physician's report will contain a crucial piece of data: the Permanent Impairment Rating (PIR). This percentage is the medical expert's quantification of your client's permanent loss of function. It's a number that has a direct and significant impact on the final settlement value, particularly in workers' comp cases.

The PIR isn't just an abstract figure; it's the bedrock for your damages calculation. A higher rating provides strong justification for a larger settlement, covering everything from pain and suffering to a lifetime of diminished earning capacity.

Research from the workers' compensation field shows a clear link between medical treatment and impairment ratings. While the average whole-body impairment rating is 6.5%, that number shifts dramatically based on the level of intervention. For instance, claims involving two surgeries see the average rating jump to 8.2%. For those with three or more surgeries, it climbs even higher to 11.3%—more than double the 5% baseline for injuries that didn't require surgery. This data shows just how critical it is to fight back against an unfairly low impairment rating from the defense.

To make the MMI assessment more concrete, doctors can use objective testing. A Functional Capacity Evaluation (FCE) is one of the most powerful tools for this. It’s a standardized series of tests that produces hard data on your client’s physical limitations, making it much tougher for the defense to argue that their condition isn't as severe as you claim.

Calculating the True Value of an MMI Payout

Once a doctor declares Maximum Medical Improvement, the real work begins for a PI attorney. This is the pivot point where we stop tracking active treatment and start building the case for your client's future. It's our job to translate that now-stabilized medical condition into a concrete, justifiable settlement figure that will last a lifetime.

This isn't about just adding up old medical bills. A comprehensive maximum medical improvement payout is a meticulously constructed argument, built piece by piece with hard evidence, expert opinions, and sound financial forecasting. Every single dollar must be accounted for and defended.

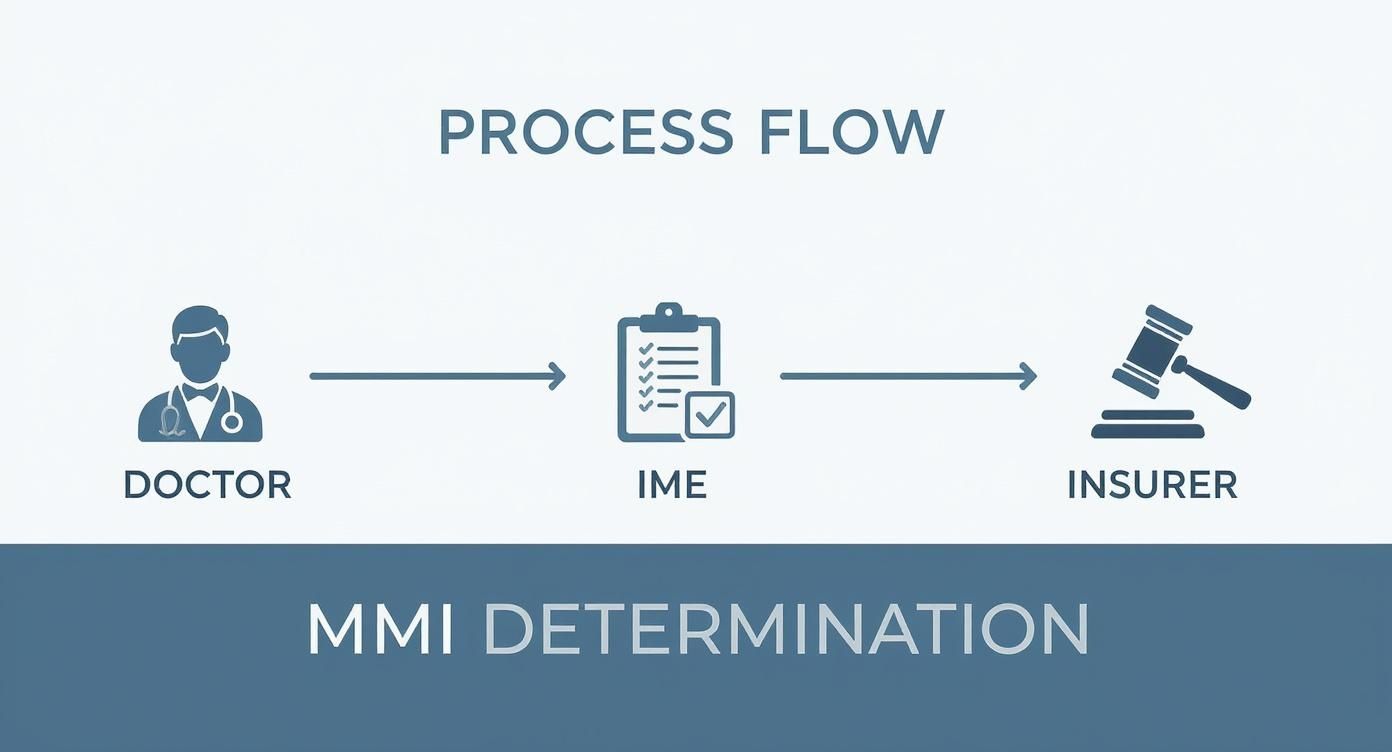

The journey to an MMI determination itself involves the treating physician, often a defense-hired Independent Medical Examiner (IME), and the insurer, each with their own perspective.

This process is a minefield. As the graphic shows, there are critical moments along the way where a case's value can either be cemented or severely undercut.

Projecting Future Medical Expenses

This is almost always the single largest component of an MMI settlement. Because MMI means the condition is permanent, we can now map out a life care plan that projects every reasonably necessary medical cost for the rest of your client's life.

This is far from guesswork; it's a methodical, evidence-based process. We need to account for:

- Ongoing Therapies: The cost of physical therapy, occupational therapy, or pain management sessions needed to maintain whatever function remains and prevent the condition from getting worse.

- Prescription Medications: A lifetime supply of all necessary drugs, with built-in adjustments for future inflation.

- Medical Equipment: The cost of wheelchairs, braces, home modifications, and other assistive devices, including the budget for replacing and maintaining them over the years.

- Potential Future Surgeries: If medical experts believe future procedures—like a joint replacement or spinal fusion revision—are probable, their costs have to be included right now.

Crucially, every one of these future costs must be converted to its present-day value. This is the lump sum of money needed today that, if invested prudently, would cover all those projected expenses as they come due. You can bet the defense will have their own experts trying to poke holes in this number.

Quantifying Economic and Non-Economic Damages

With the future medicals locked in, we then turn to calculating all the other losses that make up the final demand. These fall neatly into two buckets.

Economic Damages are the tangible, out-of-pocket financial losses your client has suffered and will continue to suffer. Think of these as the "on paper" losses.

Non-Economic Damages are meant to compensate for the very real, but intangible, human cost of the injury. These are often the most contentious part of a negotiation.

Here's a breakdown of what we're fighting for in a typical MMI payout demand.

Components of a Maximum Medical Improvement Payout Calculation

| Damage Category | Description | Calculation Method Example |

|---|---|---|

| Past Medical Expenses | All medical bills incurred from the date of injury until the MMI declaration. | Summation of all invoices, liens, and out-of-pocket receipts. |

| Future Medical Expenses | Projected costs for all future medical care, therapies, and equipment. | Life care plan valuation, reduced to present-day value using an economist's report. |

| Past Lost Wages | All income lost from the date of injury until the settlement. | Calculation of missed paychecks, bonuses, and overtime based on employment records. |

| Loss of Earning Capacity | The reduction in a client's ability to earn income over their working life. | Comparison of pre-injury and post-injury earning potential, often via a vocational expert's report. |

| Pain and Suffering | Compensation for the physical pain and mental anguish endured. | Often calculated using a multiplier (e.g., 1.5-5x economic damages) or a per diem method. |

| Emotional Distress | Damages for anxiety, depression, PTSD, and psychological trauma. | See our guide on how to calculate emotional distress damages for detailed methods. |

| Loss of Enjoyment of Life | Compensation for the inability to engage in hobbies and daily activities. | Demonstrated through client testimony, witness statements, and "before and after" evidence. |

Each category requires its own specific evidence and strategic approach to prove and maximize.

Building a powerful case for non-economic damages is about storytelling. You have to use medical records, deposition testimony, and your client’s own words to paint a clear, undeniable picture of how their life has been permanently diminished.

The financial stakes here are enormous. Back in 2007, the U.S. workers' compensation system alone covered about 132 million workers and paid out over $55 billion in benefits. That money was split almost evenly, with over $27 billion for medical care and another $28 billion in cash benefits for lost work. The average payment per claim was just $1,477, but that number masks the reality: the payouts for serious, permanent injuries are orders of magnitude higher and drive the total value of the system.

Structuring Payouts and Navigating Liens

Getting the insurance company to agree to a fair settlement number after MMI feels like a huge win. And it is. But it’s only half the battle.

How that money is actually paid out and managed is every bit as critical for your client’s long-term well-being. A poorly structured payout can trigger unexpected tax consequences or disqualify them from essential government benefits, effectively clawing back a huge chunk of your hard-won recovery.

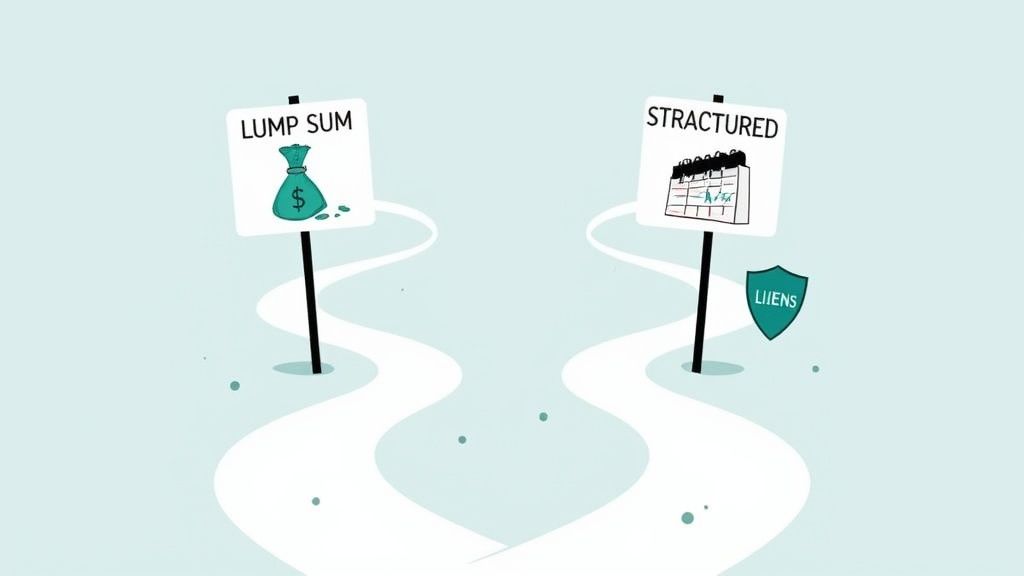

The first big decision is whether to take the money all at once in a lump sum or spread it out over time in a structured settlement. Each path has serious pros and cons, and the right answer depends entirely on your client's unique financial picture, future medical needs, and frankly, their own financial discipline. Your job is to walk them through it so they can make a choice that truly protects them.

Lump Sum vs. Structured Settlements

A lump-sum payment puts the entire settlement amount into your client's hands right away. It offers incredible flexibility. They can pay off crushing medical debt, buy a wheelchair-accessible home, or invest the funds to generate growth. The freedom is empowering.

But that freedom comes with a ton of risk. Without a rock-solid financial plan, it's frighteningly easy for a client to burn through a large settlement in just a few years, long before their medical needs have run their course.

A structured settlement, on the other hand, sets up a stream of guaranteed, tax-free payments. These can be scheduled for a certain number of years or even for the rest of the client's life. This creates a reliable financial floor, covering ongoing expenses without the risk of mismanagement or a stock market downturn wiping them out. The trade-off, of course, is that they can’t just pull out a large chunk of cash for a sudden, unexpected need.

The core question is one of security versus control. A structured settlement acts as a financial safety net, ensuring long-term needs are met, while a lump sum puts the client in complete control of their financial destiny, for better or for worse.

For clients who have never managed large sums of money or who face a lifetime of predictable care costs, that structured settlement can provide invaluable peace of mind.

The Role of Medicare Set-Asides

Things get more complicated if your client is on Medicare or is likely to be in the near future. In these cases, a Medicare Set-Aside (MSA) isn't optional—it's a requirement. An MSA is essentially a portion of the settlement that gets walled off, specifically to pay for future medical care that Medicare would otherwise have to cover.

The whole point is to protect Medicare’s interests and make sure the settlement, not the taxpayer, pays for the client’s injury-related care. If you don't set up an MSA when one is required, the consequences are severe. Medicare can deny all future claims related to the injury and can even sue to get its money back.

Figuring out the right MSA amount is a complex process. It demands a deep dive into the medical records to project the costs of all future Medicare-covered treatments. This is where meticulous organization becomes non-negotiable. For any attorney in this field, knowing how to organize medical records is a foundational skill that pays for itself ten times over when it's time to build a compliant settlement.

Identifying and Resolving Liens

Before your client sees a penny of the settlement, you have a crucial job to do: identify and resolve every single lien against their recovery. A lien is a legal IOU held by a third party that provided services or paid bills on your client’s behalf. These liens must be paid back from the settlement funds.

They can pop up from several places:

- Medical Liens: From the hospitals, surgeons, and physical therapists who treated your client with the understanding they’d be paid from the settlement.

- Governmental Liens: From programs like Medicare, Medicaid, or the VA, which have a legal right to be reimbursed for the costs they covered.

- Private Liens: From your client's own health insurance company, which likely has a "subrogation" clause in its policy allowing it to reclaim what it paid out.

Ignoring these liens is a recipe for disaster and can expose both you and your client to legal action. The final leg of any maximum medical improvement payout is a careful negotiation with these lienholders to reduce their claims and maximize what your client actually gets to take home. This final stage also involves a lot of paperwork; understanding the finer points of document notarization after car accidents can help ensure every 'i' is dotted and every 't' is crossed for a clean and compliant disbursement.

Countering Common Insurance Defense Tactics

The moment your client hits Maximum Medical Improvement, don't expect the insurance company to suddenly see the light and write a check for your full demand. It just doesn't happen. Instead, this is when their defense strategy truly kicks into high gear. They have a predictable playbook of tactics, all designed to pick apart your valuation and drive down the final payout.

Knowing their moves before they make them is half the battle. When you can anticipate their arguments, you can proactively build a case that shores up any potential weaknesses and puts them on the defensive. This approach turns the MMI milestone from a point of conflict into your single most powerful piece of negotiation leverage.

Challenging the MMI Date and Impairment Rating

The first and most predictable move is to attack the credibility of your treating physician’s opinion. Adjusters will almost always hire their own Independent Medical Examiner (IME) to create a competing narrative.

This hired gun’s report is designed to do two things:

- Push for an Earlier MMI Date: The IME will often claim your client was "as good as they were going to get" months ago, a convenient argument that attempts to invalidate any treatment that occurred after that fictional date.

- Assign a Lower Impairment Rating: The defense doctor will almost certainly assign a much lower permanent impairment rating than your client’s actual doctor did. This is a direct assault on the foundation of your future damages and non-economic damages calculations.

Your job is to dismantle this by showcasing the sheer weight of your evidence. Contrast the long-term, established relationship the treating physician has with your client against the IME's single, often brief, examination. Every piece of objective evidence—from MRIs and specialist reports to functional capacity evaluations—becomes a weapon to prove that your doctor's opinion is the one grounded in a thorough understanding of the case.

Disputing the Necessity of Future Medical Care

Next, expect the defense to paint your life care plan as an over-the-top wish list. They’ll argue the proposed future medical care is speculative, excessive, or even unrelated to the accident. It’s a classic tactic.

The goal is simple: to sow doubt and slash the largest line item in your maximum medical improvement payout demand. They might suggest cheaper (and less effective) alternatives or point to statistics about the low success rates of a necessary surgery.

A powerfully crafted demand letter is your first line of defense. It should not just list future costs but build a compelling narrative, connecting each recommended treatment directly back to the permanent injuries documented in the medical records.

The only way to win this fight is with rock-solid support from your medical experts. A detailed report or, even better, deposition testimony from the treating surgeon explaining precisely why a specific procedure is medically necessary is invaluable. This expert testimony re-frames the conversation from one of optional care to one of essential maintenance—treatment required to prevent the client's condition from getting worse.

At the end of the day, insurers want to close old files. It’s a financial reality. An analysis of aged workers' comp claims by Aon found that 71% had already reached MMI, and 35% of those were ready to settle. Closing these files is good for their balance sheet. Your job is to make your well-documented, evidence-heavy settlement demand the path of least resistance to getting that file off their desk.

Frequently Asked Questions About MMI Payouts

When a client's case approaches the maximum medical improvement milestone, a whole new set of questions tends to pop up. This is a critical turning point—the moment we shift from focusing on active treatment to defining the final value of a claim. It's often fraught with confusion for clients and can even trip up less experienced legal staff.

Let's clear the air and tackle some of the most common questions head-on. Getting these answers straight is essential for managing client expectations and making the right strategic moves as you head into settlement talks.

Does Reaching MMI Mean My Client Is Fully Healed?

This is the single biggest misconception out there, and it’s crucial to get ahead of it. Reaching Maximum Medical Improvement absolutely does not mean your client is cured or back to their old self. It’s simply the point at which a doctor says their condition has plateaued—it's as good as it's going to get, and further major improvements aren't expected, even with more treatment.

Frankly, MMI often marks the official recognition of a permanent injury. Your client might be facing a lifetime of chronic pain, physical limitations, or the need for ongoing maintenance care. The MMI determination is the medical system's way of giving us the green light to calculate the true, long-term cost of that permanent condition.

Think of it like this: MMI is where the narrative shifts from recovery to management. We're no longer trying to fix the injury; we're defining the permanent damage and securing the resources needed to manage it for a lifetime.

You have to walk your client through this distinction carefully. If they think MMI means their medical journey is over, the reality can be a tough pill to swallow. Make it clear that this is a legal and medical milestone for calculating their settlement, not the end of their story.

Can a Case Be Reopened After an MMI Payout?

For the vast majority of personal injury cases, once a final settlement agreement is signed and the check clears, the door slams shut. Forever. That's why we have to be so meticulous in getting the valuation right the first time around.

There are, however, some rare exceptions. In certain workers' compensation systems, for example, a claim might be reopened if a client’s condition substantially and unexpectedly worsens. But proving this is an uphill battle. You need rock-solid medical evidence directly tying the decline to the original workplace injury, and the legal bar is incredibly high.

In a standard PI settlement, though, the "full and final" release your client signs is exactly what it sounds like. This finality is why there's so much pressure to get every detail of the life care plan and future medical needs right. One mistake or oversight could leave your client uncompensated for a medical crisis years down the line.

What Happens if a Doctor Disagrees on the MMI Date?

It would be more surprising if the doctors didn't disagree. It's incredibly common to see the client's trusted treating physician on one side and the insurance company's Independent Medical Examiner (IME) on the other, with two very different opinions on the MMI date and the impairment rating.

The treating doctor, who has seen the client's journey unfold over months or even years, will naturally be more cautious. The IME, hired by the defense for a one-off exam, almost always pushes for an earlier MMI date and a lower impairment rating to minimize the insurer's exposure.

When this happens, you've got a classic "battle of the experts." Your job is to make it clear why the treating physician’s opinion is the one that holds more weight.

Here’s how you win that fight:

- Highlight the History: Drive home the contrast between the treating doctor’s extensive, hands-on relationship with the client versus the IME’s brief, 30-minute exam.

- Bring the Receipts: Back up the treating doctor’s opinion with objective evidence. MRIs, CT scans, specialist consults, and Functional Capacity Evaluations (FCEs) provide hard data that an IME can't easily dismiss.

- Depose the IME: Get the defense doctor under oath. A skilled deposition can expose their bias, poke holes in their report, and reveal just how little they actually know about your client’s day-to-day reality.

If the two sides still can't find common ground, the decision will likely come down to a mediator, an arbitrator, or a jury. In those moments, the attorney with the most organized, well-documented, and compelling medical evidence is the one who will prevail.

Building that powerful, evidence-based argument is where Ares gives your firm a decisive advantage. Instead of spending dozens of hours manually sifting through thousands of pages of medical records to find the key evidence, our AI-powered platform does it for you in minutes. Ares automatically organizes medical chronologies, identifies conflicting reports, and pinpoints the exact documentation you need to dismantle a defense IME’s opinion. Strengthen your MMI valuation and get to a better settlement faster by visiting the Ares Legal website.

To wrap things up, here are some quick-reference answers to the most common questions we encounter about MMI and the settlement process.

Frequently Asked Questions About MMI Payouts

| Question | Answer |

|---|---|

| What exactly is a Maximum Medical Improvement (MMI) payout? | It’s the portion of a personal injury settlement that compensates a client for damages after their medical condition has stabilized. It includes future medical costs, permanent impairment, lost earning capacity, and pain and suffering related to the long-term effects of the injury. |

| How does an MMI date impact the settlement amount? | The MMI date is the official point when future damages can be calculated. An earlier MMI date, favored by insurers, can reduce the valuation of future care and lost wages. A later, more accurate date supported by the treating physician typically leads to a higher, fairer settlement. |

| Can my client still receive medical treatment after MMI? | Absolutely. MMI doesn’t mean treatment stops. It means the focus shifts to maintenance care—like physical therapy, pain management, or medication—designed to manage a permanent condition, rather than cure it. The cost of this future care is a key part of the MMI payout. |

| What is an Impairment Rating and why does it matter? | An impairment rating is a percentage assigned by a doctor that quantifies the degree of permanent functional loss. It's a critical factor used to calculate the value of the non-economic (pain and suffering) and economic (lost earning capacity) damages in a settlement. |

| Should we always accept the first MMI opinion from a doctor? | No, not if it's from a defense IME or seems premature. If the client is still showing signs of improvement or their condition is unstable, it's crucial to challenge an early MMI determination. Securing a second opinion or pushing back with evidence is often necessary. |

Hopefully, this table provides a handy cheat sheet for you and your team. Having a firm grasp on these concepts is fundamental to navigating the final, most critical stage of a personal injury claim.